Other Economic Issues

While currency fluctuations are probably the major economic consideration in a cross-border transaction, there are quite a few other considerations.

Repatriation of Funds: Most countries allow foreign investors to “repatriate” or take their money back home. Some do not. Some only allow a certain amount to be carried out of the country. Other countries allow for repatriations but “hard currency” may not be available. Planning for any investment should include an “exit strategy”. This is extremely important in international transactions.

Allowable Foreign Ownership: In most of the industrialized countries there are no or very few restrictions on foreign ownership. These are usually matters of reporting and paying taxes. Some countries, such as Mexico, have restrictions on properties within a certain distance of the borders or the coast. Other countries either do not allow foreign ownership or require participation by a national of that country. Frequently the restrictions can be avoided by using a domestic artificial entity such as a corporation, anonymous society, LLC, trust or partnership. The artificial entity may need a portion of foreign ownership as well.

In certain cases, like China, no one can actually own the land. They can only lease it from the government. This is true in specific situations in other countries. In Russia the land outside the cities can be owned by a domestic entity. Land inside the cities is owned by and leased from the city. In Israel, a lot of the land is owned by the Israel Land Agency and leased from them. In these cases the individual only owns the improvements.

Taxation: This can be an extremely complicated issue. Buyers should always talk to a local tax attorney specializing in working with nationals of their own county. Frequently there are special permits required for foreign buyers or sellers. A foreign buyer potentially becomes a foreign seller. The time to examine taxes is before purchase. Tax treaties are also extremely important in the treatment of foreign buyers, sellers and owners. Occasionally governments offer special incentives to foreign companies and individuals to stimulate investment. This possibility should be examined as a standard part of the planning process.

Transfer expenses: Taxes are a major transfer expense in many places; but they are not the only transfer expense. In some countries the cost of buying or selling a property are very low. In other places they are quite expensive. Often it is good to have an artificial entity that owns each property. It may be cheaper to sell the entity than the property.

Possibility of Nationalization: This threat is not limited to the developing world. Eminent domain is the law in most countries. In some countries taking is subject to due process in other cases it is not. Australia has a reputation for not paying fair value. Venezuela takes land that the president considers to be “under-utilized”. In Zimbabwe all the land owned by whites was just taken. These are only a few examples. In the USA in Connecticut, land was taken for homeowners to sell to a commercial developer.

Tomorrow, I will travel. If a post is made it will concern other risks of owning foreign real estate and how to deal with them. If not the next post will deal with the future of international real estate. Your comments and thoughts on this subject would be appreciated.

David Segrest is a REALTOR in Charlotte, NC

David S. Segrest, CIPS, CCIM, TRC, CEA

david@segrestrealty.com

http://www.segrestrealty.com

Serving the world in the Carolinas, Serving the Carolinas in the World

Tuesday, July 17, 2007

Sunday, July 15, 2007

Currency issues for expats

Currency issues for Expatriates

People who live and work abroad

People leave their own countries to work for various reasons. This reason sometimes has a lot of influence on the way currency fluctuations affect them. There are three basic types of people working abroad. One group works for a company in their home country and is sent overseas for a long or short-term assignment. Some people work for a foreign company in the home country of their employer. Another group works for a foreign company in a country outside of the company’s home country. The ongoing obligations of the expatriate in the home country can be harmed by a negative trend in the currency of their remuneration. A positive trend may be helpful.

Sometimes expatriates are paid in the currency of their home country. In that case a negative trend of the host country could be beneficial and a positive trend could be harmful.

Some people work abroad as a way to subsidize international travel. Teaching English is a popular job for people from the USA, Great Britain, Australia, South Africa and other English speaking countries. The pay is low; but fluency in the foreign language is usually not required and living expenses are usually covered. Working with churches or international aid organizations is also popular.

Often the people who take these jobs are young people or retired people and are able to leave home with very minimal financial responsibility. One thing that makes this type of job attractive is that it affords an opportunity to interact with the local people and build relationships. The access granted is much different that the access given to a tourist.

When working abroad the employee has to deal with tax issues as well as currency issues. A person interested in taking advantage of this option should carefully research the full economic impact. A good starting place is to find and read the tax treaties between the two countries. Often, spending more than a certain number of days in a country will cause the expatriates worldwide income to be subject to tax in more than one country.

There are many other issues to consider when looking for employment abroad. These will be discussed in depth in the week beginning July 23rd. The next column will discuss economic issues other than currency.

David Segrest is a REALTOR in Charlotte, NC

David S. Segrest, CIPS, CCIM, TRC, CEA

david@segrestrealty.com

http://www.segrestrealty.com

Serving the world in the Carolinas, Serving the Carolinas in the World

People who live and work abroad

People leave their own countries to work for various reasons. This reason sometimes has a lot of influence on the way currency fluctuations affect them. There are three basic types of people working abroad. One group works for a company in their home country and is sent overseas for a long or short-term assignment. Some people work for a foreign company in the home country of their employer. Another group works for a foreign company in a country outside of the company’s home country. The ongoing obligations of the expatriate in the home country can be harmed by a negative trend in the currency of their remuneration. A positive trend may be helpful.

Sometimes expatriates are paid in the currency of their home country. In that case a negative trend of the host country could be beneficial and a positive trend could be harmful.

Some people work abroad as a way to subsidize international travel. Teaching English is a popular job for people from the USA, Great Britain, Australia, South Africa and other English speaking countries. The pay is low; but fluency in the foreign language is usually not required and living expenses are usually covered. Working with churches or international aid organizations is also popular.

Often the people who take these jobs are young people or retired people and are able to leave home with very minimal financial responsibility. One thing that makes this type of job attractive is that it affords an opportunity to interact with the local people and build relationships. The access granted is much different that the access given to a tourist.

When working abroad the employee has to deal with tax issues as well as currency issues. A person interested in taking advantage of this option should carefully research the full economic impact. A good starting place is to find and read the tax treaties between the two countries. Often, spending more than a certain number of days in a country will cause the expatriates worldwide income to be subject to tax in more than one country.

There are many other issues to consider when looking for employment abroad. These will be discussed in depth in the week beginning July 23rd. The next column will discuss economic issues other than currency.

David Segrest is a REALTOR in Charlotte, NC

David S. Segrest, CIPS, CCIM, TRC, CEA

david@segrestrealty.com

http://www.segrestrealty.com

Serving the world in the Carolinas, Serving the Carolinas in the World

Thursday, July 12, 2007

Currency Trends and Retirees

Currency Trends and Retirees

A major result of globalization is that people everywhere in the world learn more about other parts of the world. This has caused many people to realize that there could be advantages to retiring abroad. For some people it is the environment such as beaches, mountains, or access to activities. For other people the driving reason is financial. They can live a much better lifestyle with the fixed income they have in retirement.

The decision to retire abroad can be difficult. If a retiree buys a home in an area where prices don’t increase or where properties are hard to sell, it could tie up or endanger a big part of their retirement nest-egg. The retiree may find that children, grandchildren and friends do not come to visit or do not come as often. Sometimes there are medical issues.

On the other hand there can me many benefits. Taking advantage of a favorable currency trend can be one of them. For example:

The Nicaraguan Cordoba has lost value against the US$ at the rate of about 5% per year since 2002. This would mean an increase in income for someone with a dollar-based retirement fund of 5% per year. That same person, living in the USA would have seen their purchasing power diminish because of inflation. In order to make a true comparison one would need to compare the inflation rate in Nicaragua. How effective are official inflation rates. If the Cordoba had improved the retiree would have lost even more purchasing power.

Governments have a tendency to make these rates appear artificially low; because of their effects on entitlement programs and the appearance of their economy and government. The only way to really measure inflation on a personal basis is to examine the personal budget. Find some old newspapers and discover what the cost would have been at some point in the past and then compute the change to the present time.

In the case of Nicaragua, the price of fresh vegetables and meats is considerably cheaper than in the USA. Real estate in exotic locations is not a great deal cheaper. If the retiree is content to live in a property similar to what the local inhabit, a really nice home can be had for considerably less than in the USA. It may be a really good idea, wherever one retires, to rent a home for 6 months or a year and get used to living in the new location and get familiar with the neighborhoods and the markets. It may be possible to find a job in the new environment and really get to know some people there.

In the first episode of this blog “What and Why”, working abroad was not mentioned as a reason for buying international real estate. That was a serious omission. The next blog will discuss the currency implications of that.

Concerning future postings…Next Tuesday, I will go to Chicago. On Wednesday and Thursday I will participate in a National Association of REALTORS (NAR) Presidential advisory group meeting on the Future of International Real Estate and NAR’s position in that future. The posting for those days will focus on what I learn. Friday and Saturday I will teach an “International Real Estate for Local Markets Course” for the Las Vegas Assn. of REALTORS. I will report on international real estate investment in Nevada on those days. The following week the topic will be working abroad as a form of subsidized travel. I will ask some friends who have more knowledge about that subject to make some guest blogs.

David Segrest is a REALTOR in Charlotte, NC

David S. Segrest, CIPS, CCIM, TRC, CEA

david@segrestrealty.com

http://www.segrestrealty.com

Serving the world in the Carolinas, Serving the Carolinas in the World

A major result of globalization is that people everywhere in the world learn more about other parts of the world. This has caused many people to realize that there could be advantages to retiring abroad. For some people it is the environment such as beaches, mountains, or access to activities. For other people the driving reason is financial. They can live a much better lifestyle with the fixed income they have in retirement.

The decision to retire abroad can be difficult. If a retiree buys a home in an area where prices don’t increase or where properties are hard to sell, it could tie up or endanger a big part of their retirement nest-egg. The retiree may find that children, grandchildren and friends do not come to visit or do not come as often. Sometimes there are medical issues.

On the other hand there can me many benefits. Taking advantage of a favorable currency trend can be one of them. For example:

The Nicaraguan Cordoba has lost value against the US$ at the rate of about 5% per year since 2002. This would mean an increase in income for someone with a dollar-based retirement fund of 5% per year. That same person, living in the USA would have seen their purchasing power diminish because of inflation. In order to make a true comparison one would need to compare the inflation rate in Nicaragua. How effective are official inflation rates. If the Cordoba had improved the retiree would have lost even more purchasing power.

Governments have a tendency to make these rates appear artificially low; because of their effects on entitlement programs and the appearance of their economy and government. The only way to really measure inflation on a personal basis is to examine the personal budget. Find some old newspapers and discover what the cost would have been at some point in the past and then compute the change to the present time.

In the case of Nicaragua, the price of fresh vegetables and meats is considerably cheaper than in the USA. Real estate in exotic locations is not a great deal cheaper. If the retiree is content to live in a property similar to what the local inhabit, a really nice home can be had for considerably less than in the USA. It may be a really good idea, wherever one retires, to rent a home for 6 months or a year and get used to living in the new location and get familiar with the neighborhoods and the markets. It may be possible to find a job in the new environment and really get to know some people there.

In the first episode of this blog “What and Why”, working abroad was not mentioned as a reason for buying international real estate. That was a serious omission. The next blog will discuss the currency implications of that.

Concerning future postings…Next Tuesday, I will go to Chicago. On Wednesday and Thursday I will participate in a National Association of REALTORS (NAR) Presidential advisory group meeting on the Future of International Real Estate and NAR’s position in that future. The posting for those days will focus on what I learn. Friday and Saturday I will teach an “International Real Estate for Local Markets Course” for the Las Vegas Assn. of REALTORS. I will report on international real estate investment in Nevada on those days. The following week the topic will be working abroad as a form of subsidized travel. I will ask some friends who have more knowledge about that subject to make some guest blogs.

David Segrest is a REALTOR in Charlotte, NC

David S. Segrest, CIPS, CCIM, TRC, CEA

david@segrestrealty.com

http://www.segrestrealty.com

Serving the world in the Carolinas, Serving the Carolinas in the World

Wednesday, July 11, 2007

Investors and Currency Trends

Investors and Currency Trends

In currency as well as in stock prices, the old adage “The trend is your friend”, is very applicable. Currency risk can be planned for by examining the trends. In the chart from the last blog, the trends of the different currencies show a definite pattern in a certain direction. In one instance between the Argentine peso and the other currencies there is a huge differential. It is imperative that when using trends to make investment projections, any “blips” like this must be studied to find underlying causes.

In this particular case, the peso had been pegged to the US$; and the peg had been dropped because of an economic crisis in Argentina. Many times when there are large fluctuations of this nature a longer term trend can be examined to get a better understanding. That would not be helpful in this instance because the peso had been pegged to the dollar and the old data would only show a level relationship. In general, investors like to see the currency of the target investment country improve against their own currency. This means that the return on their investment will increase because of the currency trend. The exception might be a highly leveraged investment in which the mortgage is denominated in the target countries currency. Any negative cash flows would result in a higher cost for the investor as the deficits were covered from the home country.

A really great example of currency trends causing problems for investors is Hawaii in the ‘80s. The Japanese were able to borrow money in Japan very cheaply. They borrowed money to buy hotels in Hawaii at a very low yield and a very high loan to value ration (LTV). As the yen increased in value against the dollar and the yield from the hotels dropped, repaying the debt on the mortgages became increasingly difficult. Not only were the individual investors harmed, the entire Japanese banking system suffered. The Japanese banking system is enduring upheavals today as a result of these old problems. The next blog will deal with currency trends and retirees.

David Segrest is a REALTOR in Charlotte, NC

David S. Segrest, CIPS, CCIM, TRC, CEA

david@segrestrealty.com

http://www.segrestrealty.com

Serving the world in the Carolinas, Serving the Carolinas in the World

In currency as well as in stock prices, the old adage “The trend is your friend”, is very applicable. Currency risk can be planned for by examining the trends. In the chart from the last blog, the trends of the different currencies show a definite pattern in a certain direction. In one instance between the Argentine peso and the other currencies there is a huge differential. It is imperative that when using trends to make investment projections, any “blips” like this must be studied to find underlying causes.

In this particular case, the peso had been pegged to the US$; and the peg had been dropped because of an economic crisis in Argentina. Many times when there are large fluctuations of this nature a longer term trend can be examined to get a better understanding. That would not be helpful in this instance because the peso had been pegged to the dollar and the old data would only show a level relationship. In general, investors like to see the currency of the target investment country improve against their own currency. This means that the return on their investment will increase because of the currency trend. The exception might be a highly leveraged investment in which the mortgage is denominated in the target countries currency. Any negative cash flows would result in a higher cost for the investor as the deficits were covered from the home country.

A really great example of currency trends causing problems for investors is Hawaii in the ‘80s. The Japanese were able to borrow money in Japan very cheaply. They borrowed money to buy hotels in Hawaii at a very low yield and a very high loan to value ration (LTV). As the yen increased in value against the dollar and the yield from the hotels dropped, repaying the debt on the mortgages became increasingly difficult. Not only were the individual investors harmed, the entire Japanese banking system suffered. The Japanese banking system is enduring upheavals today as a result of these old problems. The next blog will deal with currency trends and retirees.

David Segrest is a REALTOR in Charlotte, NC

David S. Segrest, CIPS, CCIM, TRC, CEA

david@segrestrealty.com

http://www.segrestrealty.com

Serving the world in the Carolinas, Serving the Carolinas in the World

Tuesday, July 10, 2007

Currency Trends

Currency Trends

Although currency issues may be minor relative to other considerations for vacation home buyers, for investors and retirees they may be the single most important factor. For the investor the currency trends will determine where and when to invest. For the retirees the currency trend will determine where they wish to stash their nest egg and in what currency it should be denominated.

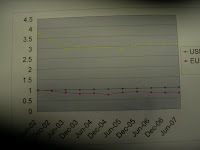

There are several websites that give current and historical data on currency exchange rates. One is http://www.oanda.com/ . That is the converter used to obtain the historical data for the following chart. In this chart the US$, The Euro, and the Argentina Peso are compared. The dollar is used as the standard and is always “1”.

Although currency issues may be minor relative to other considerations for vacation home buyers, for investors and retirees they may be the single most important factor. For the investor the currency trends will determine where and when to invest. For the retirees the currency trend will determine where they wish to stash their nest egg and in what currency it should be denominated.

There are several websites that give current and historical data on currency exchange rates. One is http://www.oanda.com/ . That is the converter used to obtain the historical data for the following chart. In this chart the US$, The Euro, and the Argentina Peso are compared. The dollar is used as the standard and is always “1”.

A chart is valuable for understanding a trend because it makes movements visible. Remember that when the exchange rate of one currency drops against another currency that means that the currency is getting stronger.

This chart shows represents the exchange rates as of 6/29 and 12/29 from 6/29/02 to 6/29/07. One can see that both currencies have gained strength against the dollar since that time. Looking at a chart separately from the current events of the time can cause misperception. The Argentine peso had just been devalued and the currency was in crisis at the beginning of the chart. After its recovery the peso has actually been remaining steady against the $ and losing significantly against the Euro.

What are the indications for investors? What are the indications for retirees who receive a pension from any of the three countries and live in another? These questions will be discussed in the next blog. What do you think?

David Segrest is a REALTOR in Charlotte, NC

David S. Segrest, CIPS, CCIM, TRC, CEA

david@segrestrealty.com

http://www.segrestrealty.com/

Serving the world in the Carolinas, Serving the Carolinas in the World

Tuesday, July 3, 2007

Risk in International Real Estate

Risk in International Real Estate

Domestic investors find market risk and credit risk to be their primary safety concerns in the USA. Whenever investors cross international borders these risks are usually increased and other risks are added as well. Some of the risks considered are property risk, political risk, economic risk, currency risk, title risk and personal risk (to the owner or others).

A basic rule of international investment is that “Capital flows to the highest yield with the lowest risk.” The perceived risk will influence the yield that an investor requires. In many markets information is very difficult to obtain or unreliable. This also increases the risk premium in most cases.

In the more sophisticated markets insurance is available to deal with property risk. These policies are often limited in ways that may cause the risk to remain with the property owner. Sometimes insuring against these risks may be cost prohibitive. Examples of property risk are flood, fire, mudslide, riot, war, adverse possession, etc. Adverse possession can be especially damaging in many areas. There are organizations such as “Campesinsos sin Tierra” that specialize in taking land by adverse possession. In most of the countries where they operate there is no political will to evict them after they have taken a property.

Political risk cannot be insured against. Eminent domain is a universal risk. Some countries pay fair value when they take properties and use a transparent process to determine the need for taking and the fair value. Other countries do not use a transparent process or sometimes do not even pay for the properties. International law requires payment for properties that are nationalized. Enforcing this law can be so expensive that a small property owner has no affordable access to justice. In many Latin countries, the government has the right to take “underutilized” property. In Venezuela the definition of “underutilized” has become extremely hazy.

Economic risk comes from severe changes in the economy that could cause the income from the property to disappear or become un-collectable.

Currency risk is closely tied to economic and political risk. The economy and politics of a country or a region can cause the currency to depreciate against the economy of the home country. This can seriously affect yield. The template for calculating IRR that was offered in an earlier blog, has a feature for the investor to input projected currency fluctuations. To get this template just send me an email requesting the “analysis template”.

In many areas property titles are not secure. Some countries do not even have land registries. Other countries have extremely good land registries. In Panama and Latvia for example the government guarantees title. In Greece there is no central land registry. In the USA the registries are maintained on a local basis and quality could vary from location to location. Cheap title insurance is available throughout the entire country. Title issues should be considered everywhere before property is acquired.

Personal risk can be a function of crime rate or of political instability. This risk usually carries the highest premium. The risk premium is usually based on the perception and perspective of the investor. Accurately understanding the risk in a market or sub-market can be an extremely profitable activity. Often the only way to have the necessary information is to spend time in the marketplace and know intimately all of the factors operating in that marketplace. In future blogs individual countries and markets will be discussed.

David Segrest is a REALTOR in Charlotte, NC

David S. Segrest, CIPS, CCIM, TRC, CEA

david@segrestrealty.com

http://www.segrestrealty.com

Serving the world in the Carolinas, Serving the Carolinas in the World

Domestic investors find market risk and credit risk to be their primary safety concerns in the USA. Whenever investors cross international borders these risks are usually increased and other risks are added as well. Some of the risks considered are property risk, political risk, economic risk, currency risk, title risk and personal risk (to the owner or others).

A basic rule of international investment is that “Capital flows to the highest yield with the lowest risk.” The perceived risk will influence the yield that an investor requires. In many markets information is very difficult to obtain or unreliable. This also increases the risk premium in most cases.

In the more sophisticated markets insurance is available to deal with property risk. These policies are often limited in ways that may cause the risk to remain with the property owner. Sometimes insuring against these risks may be cost prohibitive. Examples of property risk are flood, fire, mudslide, riot, war, adverse possession, etc. Adverse possession can be especially damaging in many areas. There are organizations such as “Campesinsos sin Tierra” that specialize in taking land by adverse possession. In most of the countries where they operate there is no political will to evict them after they have taken a property.

Political risk cannot be insured against. Eminent domain is a universal risk. Some countries pay fair value when they take properties and use a transparent process to determine the need for taking and the fair value. Other countries do not use a transparent process or sometimes do not even pay for the properties. International law requires payment for properties that are nationalized. Enforcing this law can be so expensive that a small property owner has no affordable access to justice. In many Latin countries, the government has the right to take “underutilized” property. In Venezuela the definition of “underutilized” has become extremely hazy.

Economic risk comes from severe changes in the economy that could cause the income from the property to disappear or become un-collectable.

Currency risk is closely tied to economic and political risk. The economy and politics of a country or a region can cause the currency to depreciate against the economy of the home country. This can seriously affect yield. The template for calculating IRR that was offered in an earlier blog, has a feature for the investor to input projected currency fluctuations. To get this template just send me an email requesting the “analysis template”.

In many areas property titles are not secure. Some countries do not even have land registries. Other countries have extremely good land registries. In Panama and Latvia for example the government guarantees title. In Greece there is no central land registry. In the USA the registries are maintained on a local basis and quality could vary from location to location. Cheap title insurance is available throughout the entire country. Title issues should be considered everywhere before property is acquired.

Personal risk can be a function of crime rate or of political instability. This risk usually carries the highest premium. The risk premium is usually based on the perception and perspective of the investor. Accurately understanding the risk in a market or sub-market can be an extremely profitable activity. Often the only way to have the necessary information is to spend time in the marketplace and know intimately all of the factors operating in that marketplace. In future blogs individual countries and markets will be discussed.

David Segrest is a REALTOR in Charlotte, NC

David S. Segrest, CIPS, CCIM, TRC, CEA

david@segrestrealty.com

http://www.segrestrealty.com

Serving the world in the Carolinas, Serving the Carolinas in the World

Monday, July 2, 2007

Yield (part 3) Beyond IRR

Yield (Part 3) Beyond IRR

Not many investors go beyond IRR in their analysis. For the cone-heads among us there are more advanced methods. One of these is called the “Financial manager’s rate of return” (FMRR). The problem with IRR is that it assumes all cash flows are reinvested at the same rate as the original investment. For example if the property yields an IRR of 11%, the 1st year’s cash flow is assumed to be invested at that same rate. That probably is not a valid assumption. There may not be enough money from this cash flow to reinvest at that rate.

The FMRR assumes that these cash flows will be placed in a bank account or a CD or some safe liquid investment until enough money is accumulated to re-invest. Hence we have the “safe rate” and the ‘reinvestment rate”. The “safe rate” is usually the amount that one would expect to receive on the smaller liquid investment. Some amount of money is determined to be enough to re-invest. When this much is accumulated at the safe rate, the return on that money is then calculated at the “re-investment rate”. The “re-investment rate” would probably be the average yield on the investor’s other investments.

This calculation could be fairly complicated. I can be done with a calculator or even with a pencil. It is more commonly done with a spreadsheet. Very few investors will be using this measure of yield.

Yield also needs to be adjusted for risk. In domestic investments, the major concerns are market risk and credit risk. There are quite a few other factors to be considered in international investments. They will be the subject of the next blog.

David Segrest is a REALTOR in Charlotte, NC

David S. Segrest, CIPS, CCIM, TRC, CEA

david@segrestrealty.com

http://www.segrestrealty.com

Serving the world in the Carolinas, Serving the Carolinas in the World

Not many investors go beyond IRR in their analysis. For the cone-heads among us there are more advanced methods. One of these is called the “Financial manager’s rate of return” (FMRR). The problem with IRR is that it assumes all cash flows are reinvested at the same rate as the original investment. For example if the property yields an IRR of 11%, the 1st year’s cash flow is assumed to be invested at that same rate. That probably is not a valid assumption. There may not be enough money from this cash flow to reinvest at that rate.

The FMRR assumes that these cash flows will be placed in a bank account or a CD or some safe liquid investment until enough money is accumulated to re-invest. Hence we have the “safe rate” and the ‘reinvestment rate”. The “safe rate” is usually the amount that one would expect to receive on the smaller liquid investment. Some amount of money is determined to be enough to re-invest. When this much is accumulated at the safe rate, the return on that money is then calculated at the “re-investment rate”. The “re-investment rate” would probably be the average yield on the investor’s other investments.

This calculation could be fairly complicated. I can be done with a calculator or even with a pencil. It is more commonly done with a spreadsheet. Very few investors will be using this measure of yield.

Yield also needs to be adjusted for risk. In domestic investments, the major concerns are market risk and credit risk. There are quite a few other factors to be considered in international investments. They will be the subject of the next blog.

David Segrest is a REALTOR in Charlotte, NC

David S. Segrest, CIPS, CCIM, TRC, CEA

david@segrestrealty.com

http://www.segrestrealty.com

Serving the world in the Carolinas, Serving the Carolinas in the World

Subscribe to:

Posts (Atom)